The management of the marine transportation trade had an increase of ordinary

profit noted in fiscal 1974, notwithstanding the decline or little growth in

the transport of oil and timber in the ocean shipping and a considerable increase

of costs mainly with respect to labor and fuel, because of a substantial increase

of income from the lasting transport contracts concluded at a high level of

freightage at the time of the boom.

In the market of marine transportation of the world, the tanker declined

sharply in 1974 and continued to be low in 1975. Thereafter, the tramper also

declined sharply, thus intensifying the aspect of depression. Such is due to

the stagnation of marine shipment and world-wide economic depression by the

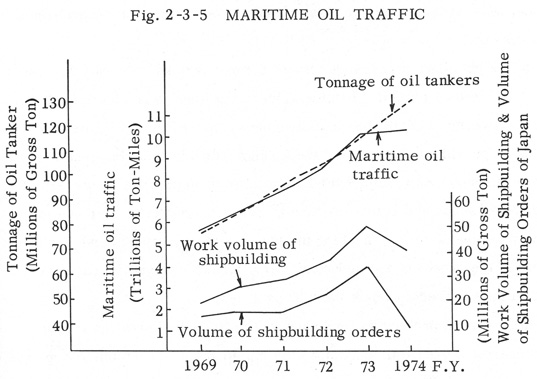

steep rise of crude oil price. Now, referring to Fig.

2-3-5, the marine shipment of oil in the world that had progressed at a

growth rate of 16 percent in ton mile basis in the past four years up to 1973,

remained at a level of 1 percent against the previous year in 1974, whereas

the tanker bottoms in the world had developed at an annual rate of 12 percent

in weight ton for the past five years and, in 1974, still maintained the high

rate of 12 percent. As the result, the excessive tanker bottoms came up on the

surface, and as of the end of June 1975, the bottoms in excess of 27,000,000

weight tons among the total bottoms of tankers in the world at about 240,000,000

weight tons are in mooring. Additionally, there are about 156,000,000 weight

tons of tankers as of the end of fiscal 1974 that were ordered to the shipyards

during the period of boom before the oil crisis, and they are further worsening

the situation.

For the market of trampers, a rapid recovery is hardly expectable on account

of inflow of ore and oil carriers due to depression of the market of tankers

and movement: to convert the tankers now ordered to bulk carriers.

On the other hand, die trend of the coastal shipping having a problem of

excessive bottoms produced with decrease of the import of and demand for timber

from the recession of the domestic market is also a big problem for the marine

transportation management.

The coastal shipping had the cargo movement decreased by 7.7 percent by

ton-kilometers against the previous year due to the recession of the domestic

market but, with rise of the freightage, was able to maintain the balance of

profit and loss. Further, with favorable turn of the balance outside the business,

it had an improved balance of ordinary profit and loss in fiscal 1974 over fiscal

1973. But, in and after the second half of fiscal 1974, it is undergoing a severe

condition because of the prolonged depression.

In the business of passenger lines, the ordinary balance rate for fiscal

1974 fell to 83.4 percent. Particularly, in the lines to remote islands for

which government subsidies are designed, it is as low as 57.3 percent.

To cope with such situation, the foreign shipping is taking such and other

measures as to adjust the bottoms through operation of tankers at a reduced

speed and laying up fleets, while the domestic shipping is advancing measures

of checking the building of new vessels and curtailment of the expenses and

reduction of the frequency of services in the case of the passenger boats including

ferries.

Such severe problems of management in the marine transportation had exerted

a great influence upon the employment of seamen, giving rise to a severe condition

for employment not seen in these years with a sharp decline of the ratio of

job offers to applicants.

Further, the foregoing trend of the marine transportation is also exerting

a direct influence upon the shipbuilding trade. Particularly, the excessive

bottoms in the global scale is expected to last for a considerable time to come,

and the effects upon the shipbuilding trade of our country building about 50

percent of the vessels newly built in the world are by no means small.

The shipbuilding trade of our country had, as of the end of fiscal 1974,

a work volume of shipbuilding of about 40,000,000 gross tons (35 major shipyards)

or for about 2.5 years. But, due to the extreme decrease of orders in fiscal

1974 (72.3 per cent decrease against the previous year) and cancellation of

some of the orders received, the work volume decrease by 20 percent against

the same term in the previous year. With the work volume of fiscal 1974 taken

as 100, it is anticipated that the work volume will decline to 70 in fiscal

1976 and to 50 in fiscal 1977.

The shipbuilding trade is thus trying to adjust the excessive labor force

by such measures as to stop the new employment, control the overtime works and

transfer the personnel to the other divisions and, at the same time, develop

new demands. But, some of the smaller shipbuilding enterprises, subcontractors

and industries related to the shipbuilding are already experiencing the effects

in the form of decreased work volume or execution of layoff.

{kind=link}