1. Present evaluation ten years after the JNR reform

(1) Purpose of the JNR reform : regenerating JNR operations

The JNR reform aimed to transform JNR, which was on the verge of collapse,

into a business entity that can survive fierce competition and to regenerate

JNR operations so as to work in a responsible manner. To realize this objective,

the single nation-wide management structure under the corporation system was

reviewed. Then JNR was split and privatized. The passenger section was divided

into six companies by region, and the freight section turned into a single nation-wide

business entity that operates on lines owned by the passenger companies with

a fee.

JR East, JR West, JR Tokai and JR Freight received a part of the long-term

debts commensurate with their book values. Other debts were supposed to be repaid

by with revenues gained from selling land and stocks owned by the Settlement

Corporation. The amount of debts that are to remain unsettled eventually, it

has been decided, will be borne by the public.

(2) Positive points : maintenance of the level of fares, improvements in

transportation services, reduced taxpayer burden, reduction of the number of

employees

Fares have basically been kept at the same levels as before the privatization

of the Japanese National Railways so as to be competitive in the transportation

market. Improvements in transportation services include achievements

such as faster transportation speeds and better customer service. However, improvements

have not kept pace with congestion and other problems. Further efforts are required

to solve these problems.

Regarding taxpayer burden, tax payments by Japan Railway companies continue

to exceed the government subsidies they receive. In this respect, JNR reform

has helped the government improve its fiscal performance, serving to ease the

burden on taxpayers.

The number of employees was reduced from 387,000 at the end of fiscal year

1982, when the plans to divide and privatize JNR was made public, to 199,000

at the end of fiscal year 1987 upon the inauguration of the JR companies, and

further to 189,000 at the end of fiscal year 1995, contributing to an improvement

in productivity.

(3) Evaluation of the JR companies : establishment of sound management foundation

is the common goal.

Each JR company should achieve the objective of the JNR reform, i.e. full-fledged

privatization as soon as possible with further efforts to increase revenue and

reduce expenditure regarding railway services. It is also necessary to further

strengthen the management foundation Jay diversifying business operations.

(A) JR East, JR West and JR Tokai : development of facilities for easing

congestion and improvement of other less developed fields are hoped for

The three companies are encouraged to ease congestion and improve less developed

fields. As in the cases of JR East and JR West, it is necessary for JR Tokai

to prepare for being listed on the stock exchange.

(B) JR Hokkaido and other two JR companies : it is urgently required to

cope with the reduction in management profit of the Management Stabilization

Funds

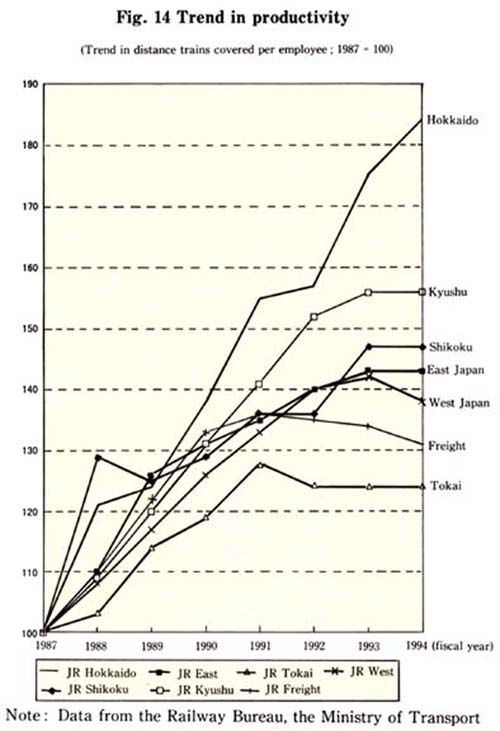

JR Hokkaido, JR Shikoku and JR Kyushu (hereinafter referred to as "JR Hokkaido"

and the other two JR companies) have seen a significant increase in productivity

(.Fig 14). However, their management

situations remain tough mainly due to a reduction in management profit of the

Management Stabilization Funds caused by low interest rates. It is therefore

necessary to make further efforts to increase revenue and rationalize management

so as to realize full-fledged privatization.

(C) JR Freight : strengthening of the management foundation is urgently

needed

JR Freight has been faced with tough management situations, recording ordinary

losses for three consecutive years from FY1993. However, the company is beginning

to specialize in fields where the characteristics of railway freight can demonstrate

itself ; it has been expanding the share of containers and speeding up freight

transport since the age of JNR. In future, it is necessary to become thoroughly

streamlined and develop transport products that are more competitive. The company

also needs to sharpen its competitive edge by establishing closer cooperative

relations with express companies so as to strengthen its management foundation.

2. Problems remaining to be solved

(1) Settlement of long-term debts and other liabilities

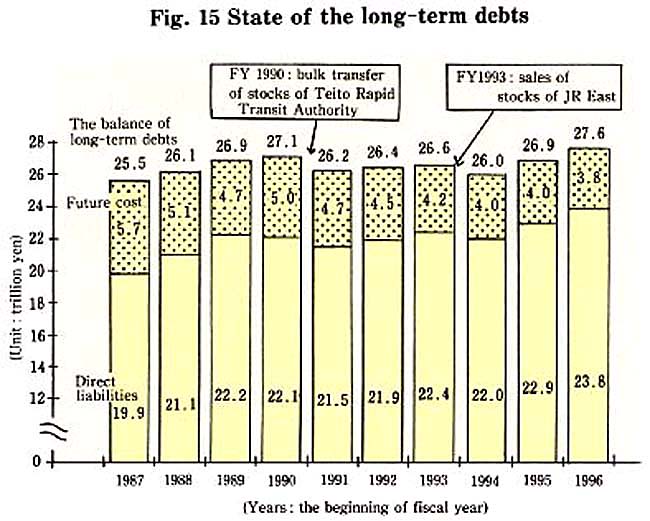

(A) State of long-term debts and other liabilities : amounted to \27. 6

trillion at the beginning of fiscal 1996

The Settlement Corporation earned 11.3 trillion yen for the nine years between

FY1987 and FY1995 but spent 13.3 trillion yen on interest payments and others

during the same nine-year period. As a result, the balance of long-term debts

and other liabilities rose from 25.5 trillion yen upon the inauguration of the

JR companies to 27.6 trillion yen.

The assets at the beginning of fiscal 1996 includes some 3 trillion yen

of land, JRS Stocks (0.3 trillion yen at face value), and about 1.9 trillion

yen of credit to the Railway Development Fund.

(B) Factors contributing to the expansion of debts : burden of interest

rates and mutual pensions

(a) Burden of payments on interest and mutual pensions The Settlement Corporation

is tackling the problem of the burden of payments on interest and mutual pensions

(hereinafter referred to as interest and other burdens). The amount of interest

incurred every year stands at 1.3-1.5 trillion yen. The balance of debts decreased

only in FY1990 and FY1993 (Fig.

15, Fig. 16).

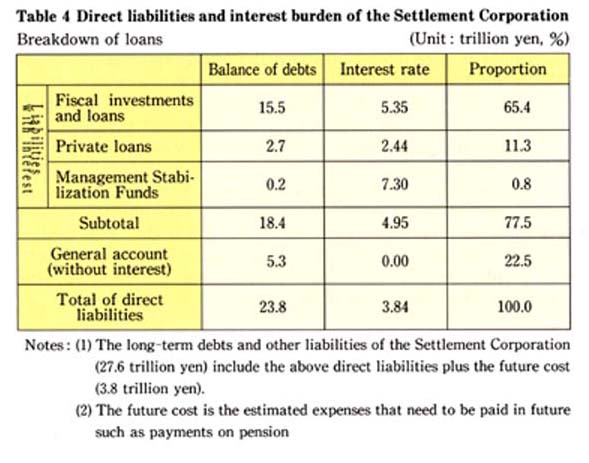

At the beginning of fiscal 1996, the liabilities with interest of the Settlement

Corporation amounted to 18.4 trillion yen with the average interest rate at

4.95% (Table 4).

(b) Burden of mutual pension fund

The Settlement Corporation shoulders a total of 700 billion yen as a special

burden concerning the Japan Railway Mutual Pension Fund. Upon integrating the

railway mutual pension into the welfare pension, the corporation plans to bear

an additional 0.8 trillion yen of liabilities in transferring money at the beginning

of fiscal 1997.

(C) Attempt to reduce debts : sales of assets and financial support

(a) Revenue from selling assets

Sales of assets such as land and stocks have not been proceeding smoothly

due to unfavorable effect of the market.

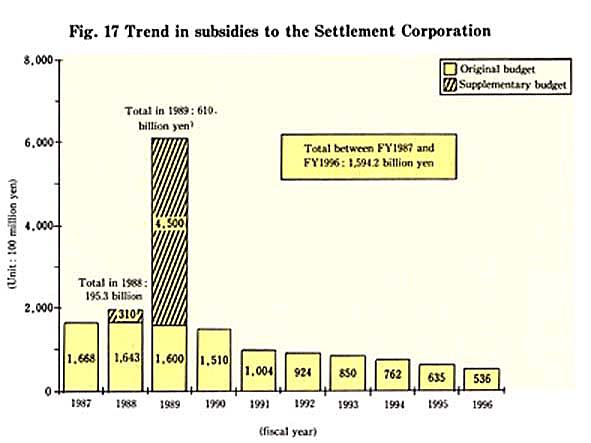

(b) Subsidies

The subsidies have totalled about 1.6 trillion yen for ten years until FY1996

(Fig. 17).

(c) Government loans without interest

The liabilities of the Settlement Corporation include loans without interest

from the general account. However, in light of the tough situation, the terms

of loans have been changed.

(D) Limitation of the present scheme : as the remaining assets decrease,

accumulation of liabilities is inevitable.

In light of the fact that the assets are decreasing, substantial reduction

in liabilities is not expected. Moreover, accumulation of liabilities is inevitable

even if the self-sponsored funds are used.

(E) Necessity of establishing measures for full-scale settlement

A delay in the full-scale settlement of liabilities will increase the financial

burden on the people. To avoid this, it is necessary to urgently establish measures

for full-scale settlement. Specific measures that can win the understanding

of the people will be wholeheartedly examined.

(2) Strengthening of the management foundation of JR Hokkaido, JR Shikoku,

JR Kyushu and JR Freight for full-fledged privatization To realize full-fledged

privatization, which is the ultimate goal of the JNR reform, following JR East,

JR West and JR Tokai, it is necessary to cope with the above-mentioned situations

by making utmost efforts to be competitive and addressing the following problems.

(A) Problems of JR Hokkaido, JR Shikoku and JR Kyushu : securing of funds

for capital investment and of management profit of the Management Stabilization

Funds

(a) Securing of funds for capital investment

Investment is needed for upgrading transportation services such as speeding

up trains because competition is intensifying with other transportation means

within the geographical domains of the three companies. However, because the

management situation of the three companies is as it is, the funds on hand are

not enough. How to deal with this problem is, a major challenge.

(b) Securing of management profit of the Management Stabilization Funds

Despite their utmost efforts, the management situation of the three companies

is deteriorating because the management profit of the Management Stabilization

Funds is decreasing due to low interest rates in recent years. Therefore it

is necessary to establish measures to secure such profit of the funds for full-fledged

privatization.

(B) Addressing problems of JR Freight : clarifying steps toward full-fledged

privatization Based on the recognition that it is necessary to clarify steps

toward full-fledged privatization, the "Roundtable on Examination of Basic Problems

for Complete Privatization of JR Freight" was held on October 11 under the direction

of the Minister of Transport. Experts and people concerned have begun to discuss

all the basic problems concerning the management of the company.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}