1. What is the Refund Method?

Under the Tax-Free Shopping System effective until October 31, 2026, eligible tax-free goods purchasers such as foreign visitors (referred to below as “purchasers”) have been exempted from consumption tax at the time of purchase at tax-free shops and have been able to buy items at tax‑exclusive prices (tax‑free).

However, for purchases made on or after November 1, 2026, the system will shift to the Refund Method, under which the amount equivalent to consumption tax will be refunded after a customs inspection at the airport or seaport confirms that the goods are being taken out of Japan.

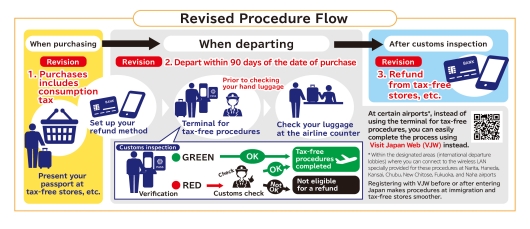

○Purchasers will buy tax-free goods at tax‑inclusive prices at tax‑free shops.

○The amount equivalent to consumption tax will be refunded after the customs inspection upon departure.

* Tax-Free Shopping System — Refund Method Leaflet (For Travelers)

<Customs Inspection upon Departure>

○ To receive the tax exemption, you must undergo a customs inspection when departing Japan.

Within 90 days from the date of purchase, you are required to present your passport at a tax‑free procedure terminal (kiosk terminal or electronic terminal) installed at airports or seaports to complete the inspection.

○ After presenting your passport, the terminal will display whether a customs inspection is required:

・If no inspection is required (Green Result), the customs inspection procedure is complete.

・If inspection is required (Red Result), you must bring your tax‑free goods to the designated customs inspection area for verification.

* At major airports with many travelers (Narita, Haneda, Kansai, Chubu, Fukuoka, New Chitose, and Naha), in addition to the tax‑free procedure terminals installed at the airport, you may also complete the process online via Visit Japan Web within areas of the international departure lobbies where dedicated Wi‑Fi wireless LAN specially for these procedures is provided (up to the security checkpoint).

* For details on Visit Japan Web, please refer to the relevant information.

<Location of Customs Inspection>

○ Tax‑free procedure terminals and customs inspection areas are installed in the international departure lobby before baggage check‑in at each airport or seaport.

<Important Notes Regarding Customs Inspection>

○ When presenting your passport at the tax‑free procedure terminal, you must have all of your purchased tax‑free goods with you.

Therefore, you cannot complete the procedure after checking in your luggage at the airport or seaport.

In addition, you cannot retrieve luggage once it has been checked in with the airline for the purpose of completing the tax‑free procedure.

○ You must complete the customs inspection (including the inspection itself if required) before completing your boarding (or embarkation) procedures, so please arrive at the airport or seaport with sufficient time.

If you abandon the inspection due to your own circumstances—such as not having enough time to complete it before boarding—the customs inspection will be considered not completed.

Please note that if you are unable to depart due to insufficient time for the tax‑free procedures, neither the airline nor Customs will provide compensation.

○ If you are departing Japan by transferring from a domestic flight to an international flight, you must complete the procedures at the airport from which you depart Japan (your final departure point).

○ If you travel on a cruise ship that departs from Japan, calls at ports overseas, and then returns to Japan, and subsequently depart Japan by air from a domestic airport (the so‑called “fly & cruise” itinerary), you must complete the procedures at the airport from which you depart Japan.

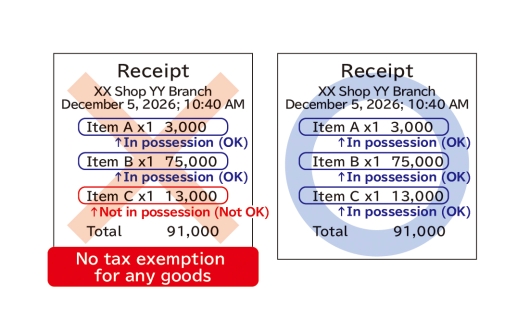

○ Customs inspections are conducted per each purchase transaction (such as a receipt). If you are not in possession of even one item included in a single purchase transaction (such as a receipt), none of the tax-free goods associated with that receipt will be eligible for customs inspection (tax refund).

○ If you have consumed all or part of your purchased tax‑free goods before departure (such as food or beverages) and no longer have them in your possession, do not complete the tax-free procedures; instead, report the consumption to a customs officer at the counter.

○ You must export the tax‑free goods that have passed the customs inspection without delay.

If you fail to export them, an amount consumption tax equivalent to the exempted consumption tax shall be collected, and you will be subject to penalties.

<Tax‑Free Goods> * Effective from November 1, 2026

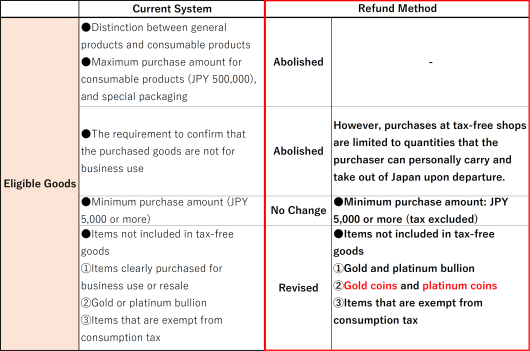

○ Purchases totaling 5,000 yen or more (tax excluded) per store per day are eligible.

1.You must take the purchased goods out of Japan.

2.Gold and platinum bullion and items exempt from consumption tax are excluded.

3.The quantity of goods must be limited to items that you can personally carry and take out of Japan at the time of departure.

4.Special packaging for consumables will be abolished; however, if consumables such as food, beverages, or cosmetics are consumed in Japan, you will not be eligible for customs inspection (tax refund).

○ The changes from the system prior to the introduction of the Refund Method (until October 31, 2026) are as follows.

* Changes to Tax‑Free Goods

However, for purchases made on or after November 1, 2026, the system will shift to the Refund Method, under which the amount equivalent to consumption tax will be refunded after a customs inspection at the airport or seaport confirms that the goods are being taken out of Japan.

○Purchasers will buy tax-free goods at tax‑inclusive prices at tax‑free shops.

○The amount equivalent to consumption tax will be refunded after the customs inspection upon departure.

* Tax-Free Shopping System — Refund Method Leaflet (For Travelers)

<Customs Inspection upon Departure>

○ To receive the tax exemption, you must undergo a customs inspection when departing Japan.

Within 90 days from the date of purchase, you are required to present your passport at a tax‑free procedure terminal (kiosk terminal or electronic terminal) installed at airports or seaports to complete the inspection.

○ After presenting your passport, the terminal will display whether a customs inspection is required:

・If no inspection is required (Green Result), the customs inspection procedure is complete.

・If inspection is required (Red Result), you must bring your tax‑free goods to the designated customs inspection area for verification.

* At major airports with many travelers (Narita, Haneda, Kansai, Chubu, Fukuoka, New Chitose, and Naha), in addition to the tax‑free procedure terminals installed at the airport, you may also complete the process online via Visit Japan Web within areas of the international departure lobbies where dedicated Wi‑Fi wireless LAN specially for these procedures is provided (up to the security checkpoint).

* For details on Visit Japan Web, please refer to the relevant information.

<Location of Customs Inspection>

○ Tax‑free procedure terminals and customs inspection areas are installed in the international departure lobby before baggage check‑in at each airport or seaport.

<Important Notes Regarding Customs Inspection>

○ When presenting your passport at the tax‑free procedure terminal, you must have all of your purchased tax‑free goods with you.

Therefore, you cannot complete the procedure after checking in your luggage at the airport or seaport.

In addition, you cannot retrieve luggage once it has been checked in with the airline for the purpose of completing the tax‑free procedure.

○ You must complete the customs inspection (including the inspection itself if required) before completing your boarding (or embarkation) procedures, so please arrive at the airport or seaport with sufficient time.

If you abandon the inspection due to your own circumstances—such as not having enough time to complete it before boarding—the customs inspection will be considered not completed.

Please note that if you are unable to depart due to insufficient time for the tax‑free procedures, neither the airline nor Customs will provide compensation.

○ If you are departing Japan by transferring from a domestic flight to an international flight, you must complete the procedures at the airport from which you depart Japan (your final departure point).

○ If you travel on a cruise ship that departs from Japan, calls at ports overseas, and then returns to Japan, and subsequently depart Japan by air from a domestic airport (the so‑called “fly & cruise” itinerary), you must complete the procedures at the airport from which you depart Japan.

○ Customs inspections are conducted per each purchase transaction (such as a receipt). If you are not in possession of even one item included in a single purchase transaction (such as a receipt), none of the tax-free goods associated with that receipt will be eligible for customs inspection (tax refund).

○ If you have consumed all or part of your purchased tax‑free goods before departure (such as food or beverages) and no longer have them in your possession, do not complete the tax-free procedures; instead, report the consumption to a customs officer at the counter.

○ You must export the tax‑free goods that have passed the customs inspection without delay.

If you fail to export them, an amount consumption tax equivalent to the exempted consumption tax shall be collected, and you will be subject to penalties.

<Tax‑Free Goods> * Effective from November 1, 2026

○ Purchases totaling 5,000 yen or more (tax excluded) per store per day are eligible.

1.You must take the purchased goods out of Japan.

2.Gold and platinum bullion and items exempt from consumption tax are excluded.

3.The quantity of goods must be limited to items that you can personally carry and take out of Japan at the time of departure.

4.Special packaging for consumables will be abolished; however, if consumables such as food, beverages, or cosmetics are consumed in Japan, you will not be eligible for customs inspection (tax refund).

○ The changes from the system prior to the introduction of the Refund Method (until October 31, 2026) are as follows.

* Changes to Tax‑Free Goods

2. Changes to Documents Required at Tax-Free Shops

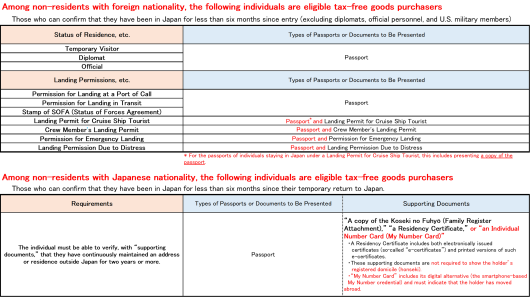

From purchases made on or after November 1, 2026, the documents required to be presented at tax‑free shops will be as follows.

* 【For Travelers】List of Eligible Tax-Free Goods Purchasers (Refund Method)

* 【For Travelers】List of Eligible Tax-Free Goods Purchasers (Refund Method)

3. Refund of the Amount Equivalent to Consumption Tax

The refund will be provided by each tax‑free shop or by a refund service provider entrusted by the shop. For details, please contact the tax‑free shop directly.

4. Frequently Asked Questions

We have prepared a Q&A section for travelers regarding the Refund Method.

Please refer to it for more information.

・Frequently Asked Questions for Travelers (Refund Method)

Please refer to it for more information.

・Frequently Asked Questions for Travelers (Refund Method)

5. Other Information / Reference Materials

・〈Japanese〉Tax-Free Shopping System — Refund Method Leaflet (For Travelers)

・〈English〉Tax-Free Shopping System — Refund Method Leaflet (For Travelers)

・〈简体中文〉Tax-Free Shopping System — Refund Method Leaflet (For Travelers)

・〈繁體中文〉Tax-Free Shopping System — Refund Method Leaflet (For Travelers)

・〈한국어〉Tax-Free Shopping System — Refund Method Leaflet (For Travelers)

・Changes to Tax‑Free Goods

・【For Travelers】List of Eligible Tax-Free Goods Purchasers (Refund Method)

・〈English〉Tax-Free Shopping System — Refund Method Leaflet (For Travelers)

・〈简体中文〉Tax-Free Shopping System — Refund Method Leaflet (For Travelers)

・〈繁體中文〉Tax-Free Shopping System — Refund Method Leaflet (For Travelers)

・〈한국어〉Tax-Free Shopping System — Refund Method Leaflet (For Travelers)

・Changes to Tax‑Free Goods

・【For Travelers】List of Eligible Tax-Free Goods Purchasers (Refund Method)